Quick Summary: Amazon’s marketplace is dominated by a mix of its own private-label Amazon Basics line alongside tech giants like Apple, consumer electronics brands, and everyday essentials. As of 2025, the best-selling brands span categories from printer paper and electronics to fashion and household goods, with Amazon Basics consistently ranking as a top performer due to aggressive pricing and Prime integration.

Amazon’s marketplace has evolved into a battlefield where established brands compete against Amazon’s own private labels for visibility and sales. With the platform generating approximately $638 billion in revenue in 2024, understanding which brands capture the largest share of buyer attention matters whether you’re a seller, competitor, or market analyst.

The brand landscape on Amazon isn’t what most people expect. While household names like Apple and Samsung maintain strong positions, Amazon’s own brands have quietly climbed to the top of bestseller lists across dozens of categories.

Amazon’s Revenue Growth and Market Position

According to SEC filings, Amazon’s aggregate market value of voting stock held by non-affiliates reached approximately $1.815 trillion as of June 30, 2024. That’s substantial growth from $693 billion in 2018 and $387 billion in 2017.

The platform’s influence on retail continues expanding. Census Bureau data shows the fourth quarter 2025 e-commerce estimate increased 5.3 percent (±1.8%) from the fourth quarter of 2024, while total retail sales grew just 2.7 percent. Amazon captures a significant portion of that digital commerce.

But here’s what’s interesting: the share of service sales in Amazon’s total net sales increased to 53% in 2022, compared to just 15% in 2012. This shift reflects the growing importance of Amazon Web Services, advertising revenue, and third-party seller fees—not just product sales.

Amazon Basics: The Quiet Dominance

Amazon Basics has become the platform’s stealth weapon. This private-label brand consistently appears in top seller positions across multiple categories.

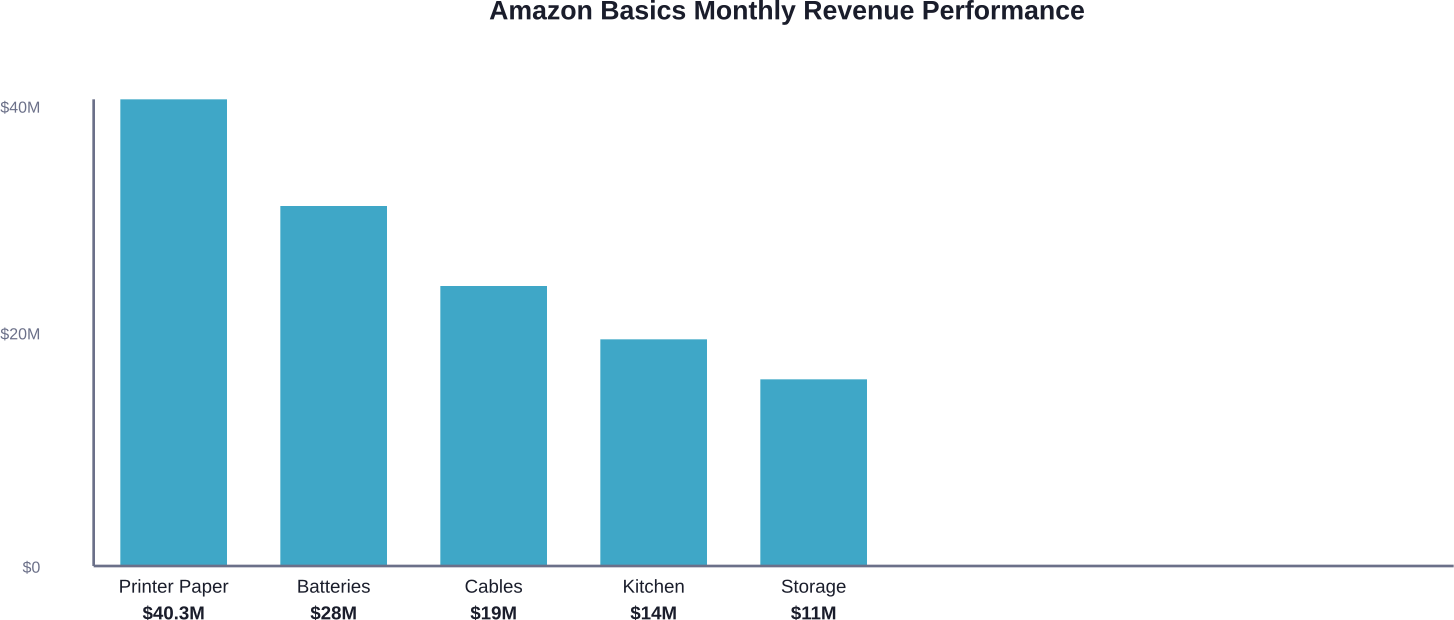

Take printer paper. Amazon Basics 20lb Copy Paper generates approximately $40.3 million in monthly sales (based on marketplace analysis data), making it one of the highest-revenue products on the entire platform. That’s not a niche success—that’s category domination.

The brand’s strategy centers on three pillars: competitive pricing that undercuts name brands by 20-40%, seamless Prime integration for fast shipping, and strategic placement in search results and recommendation algorithms.

Amazon Basics doesn’t compete in every category. The brand focuses on high-volume, low-complexity products where brand loyalty is weak and price sensitivity is high. Office supplies, batteries, cables, kitchen utensils, and storage solutions all fit this profile.

Track Amazon Advertising With WisePPC

WisePPC helps sellers analyze ad performance, keyword results, and product-level sales data in one place. It gives a clearer view of what campaigns are doing, which keywords are worth watching, and how advertising connects to product performance over time.

Need Better Visibility Into Amazon Ad Performance?

Use WisePPC to:

- analyze keyword and campaign performance

- track product sales alongside ad data

- separate paid and organic results more clearly

👉 Explore WisePPC to get a clearer view of your Amazon advertising data.

![]()

Technology Brands Leading the Pack

Apple consistently ranks among the top-selling brands on Amazon despite maintaining its own robust direct sales channels. MacBook Air, AirPods, and iPhone accessories dominate electronics bestseller lists.

The brand’s Amazon presence serves a specific purpose: capturing customers who prefer Amazon’s return policy, Prime shipping, or have Amazon gift cards. Apple products on Amazon often sell at or near MSRP, but convenience drives sales volume.

Samsung, Sony, and LG follow similar patterns in consumer electronics. These brands leverage Amazon’s massive customer base while maintaining pricing discipline to protect their brand positioning.

| Brand | Top Category | Competitive Advantage | Price Strategy |

|---|---|---|---|

| Apple | Electronics | Brand loyalty, ecosystem | MSRP maintenance |

| Samsung | Electronics, Home | Product range, innovation | Competitive pricing |

| Sony | Electronics, Gaming | Quality reputation | Premium positioning |

| Amazon Basics | Essentials, Office | Price, Prime integration | Aggressive discounting |

| Anker | Accessories, Charging | Quality-value balance | Mid-range pricing |

Fashion and Apparel Brand Performance

Clothing and footwear categories tell a different story. Amazon’s private labels like Amazon Essentials and Goodthreads compete against established brands like Levi’s, Champion, and Hanes.

Discussion in seller communities reveals that fashion brands face unique challenges on Amazon. The platform’s search algorithm prioritizes price and reviews over brand recognition, making it difficult for premium fashion brands to maintain positioning.

Athletic brands like Nike and Adidas maintain selective Amazon presence, often through authorized third-party sellers rather than direct brand stores. This strategy protects brand image while still capturing Amazon’s search traffic.

Consumer Packaged Goods and Essentials

Health, household, and beauty categories showcase a mix of established consumer brands and Amazon private labels. Brands like Crest, Tide, and Dove compete directly with Amazon’s Solimo and Happy Belly lines.

The Census Bureau noted that e-commerce sales reached over $800 billion by 2020, with substantial growth accelerating during the pandemic. This surge benefited established CPG brands that rapidly expanded their Amazon operations.

What’s changed since then? Subscription services through Subscribe & Save have become critical for CPG brand success on Amazon. Brands that optimize for recurring purchases capture higher lifetime customer value and more predictable revenue.

Emerging Direct-to-Consumer Brands

Brands that started as Amazon-native sellers have evolved into significant players. Anker, which began selling charging accessories, now generates hundreds of millions in annual revenue primarily through Amazon.

These brands understood Amazon’s ecosystem from day one. They optimized listings for search, gathered reviews aggressively, and used Amazon’s advertising platform strategically. Traditional brands entering Amazon later faced steeper learning curves.

RAVPower, TaoTronics, and similar tech accessory brands followed similar paths before some faced enforcement actions. The lesson? Amazon-native brands can scale rapidly, but compliance with platform policies remains non-negotiable.

Category-Specific Brand Dynamics

Kitchen and dining showcases interesting brand dynamics. Brands like Instant Pot became bestsellers largely through Amazon before expanding to traditional retail. The platform served as a launch pad rather than just another sales channel.

But wait. Books and media tell a completely different story. Amazon’s own publishing imprints compete directly with traditional publishers, but major publishers like Penguin Random House maintain strong bestseller presence.

Brand Value Trends

According to the Kantar BrandZ 2025 Global Top 100 ranking, Amazon’s brand value reached approximately $866 billion in 2025, growing 50% year-on-year to rank as the 4th most valuable brand globally.. This valuation reflects not just marketplace dominance but also cloud computing, advertising, and entertainment services.

For brands selling on Amazon, this concentration of power creates both opportunities and risks. Access to Amazon’s customer base offers unmatched scale, but dependence on a single platform creates vulnerability.

| Year | E-commerce Growth | Amazon Market Share | Private Label Impact |

|---|---|---|---|

| 2020 | Surge (pandemic) | Dominant position | Rapid expansion |

| 2022 | 9% YoY | Service revenue 53% | Category leaders |

| 2024 | $638B revenue | Market value $1.815T | Sustained growth |

| 2025 | 5.3% Q4 growth | Brand value undisclosed | Multi-category presence |

Geographic Variations in Brand Performance

Brand success varies significantly across Amazon’s international marketplaces. According to Forrester analysis, Amazon’s total global sales amounted to $514 billion in 2022, but regional preferences differ substantially.

European marketplaces favor local brands more strongly than the US marketplace. Amazon.de shoppers show higher loyalty to German brands, while Amazon.co.uk customers balance British and international brands differently than American shoppers.

The Role of Amazon Advertising

Advertising has become essential for brand visibility. Even top brands now invest heavily in Sponsored Products and Sponsored Brands campaigns to maintain bestseller positions.

The shift is dramatic. Brands that dominated through organic search five years ago now find that competitors who invest in advertising capture the buy box and top placements. Advertising spend has become table stakes for bestseller status.

Looking Ahead: Brand Strategy Implications

What does this landscape mean for brands considering Amazon or evaluating their current presence? Several patterns emerge.

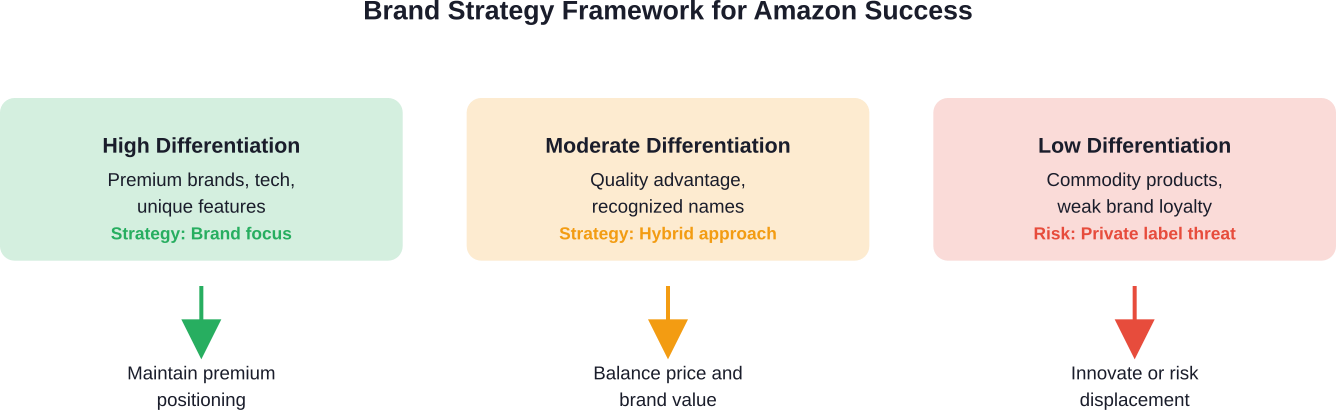

First, brands in commodity categories face intense pressure from Amazon’s private labels. Differentiation through unique features, superior quality, or strong brand loyalty becomes essential—competing on price alone rarely succeeds.

Second, technology and premium brands can maintain positioning if they provide value beyond what private labels offer. Apple succeeds on Amazon because customers want Apple specifically, not just any smartphone.

Third, Amazon-native strategies increasingly matter for traditional brands. Those that treat Amazon as just another retailer often underperform compared to brands that optimize specifically for the platform’s unique dynamics.

Real talk: the brands winning on Amazon in 2026 aren’t necessarily those with the biggest advertising budgets or longest histories. They’re the ones that understand the platform’s mechanics, adapt quickly to algorithm changes, and deliver consistent value that justifies their position in crowded categories.

Frequently Asked Questions

What brand sells the most on Amazon?

Amazon’s own private-label brands, particularly Amazon Basics, dominate sales volume across multiple categories. In electronics and technology, Apple maintains strong bestseller presence. The answer varies by category, but Amazon Basics consistently appears in top positions for office supplies, household essentials, and consumer electronics accessories.

How can I identify which brands are currently best sellers on Amazon?

Amazon updates its Best Sellers page frequently, showing top 100 products in each category. Third-party tools like Helium 10 provide sales estimates and tracking. Check category-specific bestseller lists rather than overall rankings for more accurate insights into brand performance within specific product segments.

Do Amazon’s private label brands have unfair advantages?

There is discussion among sellers suggesting that Amazon’s brands benefit from algorithm placement and access to marketplace data. Amazon maintains that all brands compete under the same search algorithm rules. Regardless of the technical details, Amazon’s private labels consistently achieve strong sales through competitive pricing and Prime integration.

Why do major brands like Apple sell through Amazon?

Apple and similar premium brands use Amazon to capture customers who prefer Amazon’s ecosystem—Prime shipping, familiar interface, gift card usage, and return policies. These brands typically maintain MSRP pricing but gain access to Amazon’s massive customer base that might not visit brand websites directly.

How has the pandemic changed which brands succeed on Amazon?

The Census Bureau noted that e-commerce sales reached over $800 billion by 2020, with acceleration during the pandemic. Brands that adapted quickly to online fulfillment, offered Subscribe & Save options, and maintained inventory during supply chain disruptions gained market share that many have retained.

What categories face the most competition from Amazon private labels?

Commodity categories with low brand loyalty face the highest private label pressure. Office supplies, batteries, charging cables, basic kitchen items, and storage solutions all see intense Amazon Basics competition. Categories requiring technical expertise, unique design, or strong brand preference remain more protected.

Is it still worth launching a new brand on Amazon in 2026?

New brands can succeed by identifying underserved niches, delivering superior quality at competitive prices, and leveraging Amazon’s advertising tools effectively. Success requires deeper pockets than five years ago due to increased advertising costs, but the platform still offers unmatched customer access for brands that differentiate effectively.

Conclusion

The best-selling brands on Amazon in 2026 reflect a marketplace where Amazon’s private labels compete alongside established consumer brands, tech giants, and emerging direct-to-consumer players. Amazon Basics dominates commodity categories through aggressive pricing and Prime integration, while brands like Apple maintain strong positions through product differentiation and brand loyalty.

For brands selling on Amazon or considering the platform, success requires understanding these competitive dynamics. Commodity products face intense pressure from private labels, making differentiation essential. Premium brands must justify their positioning with unique value. Amazon-native strategies—optimized listings, strategic advertising, review generation—have become table stakes rather than optional tactics.

The marketplace continues evolving rapidly. Brands that monitor trends, adapt strategies quickly, and maintain focus on customer value will find opportunities despite increasing competition. Those that treat Amazon as just another sales channel often struggle against competitors who’ve mastered the platform’s unique dynamics.

No credit card required

No credit card required